Health Savings Accounts (HSAs): Participation and Utilization Among U.S. Employees

Health Savings Accounts (HSAs) have emerged as a popular financial tool for managing healthcare costs in the United States. Designed to help individuals save for qualified medical expenses, HSAs are paired with high-deductible health plans (HDHPs) and offer tax advantages that make them an attractive option for many employees. This article explores the current landscape of HSA participation and utilization among U.S. employees, highlighting key statistics and trends.

What is an HSA?

An HSA is a tax-advantaged savings account that allows individuals to set aside money for healthcare expenses. Contributions made to an HSA are tax-deductible, reducing an individual’s taxable income. Additionally, withdrawals for qualified medical expenses are tax-free, and any interest or investment earnings grow tax-deferred. For 2023, the IRS allows individuals to contribute up to $3,850 for self-only coverage and $7,750 for family coverage, with an additional $1,000 catch-up contribution for those aged 55 and older.

Current Statistics on HSA Participation

1. Growth in HSA Accounts: According to the 2022 report from Devenir, the number of HSA accounts has grown significantly, reaching approximately 30 million accounts in the U.S. This represents a growth of about 10% from the previous year.- 2. Total HSA Assets: The total assets held in HSAs have also increased, with estimates nearing $100 billion in 2022. This growth indicates a rising awareness and acceptance of HSAs as a viable option for managing healthcare costs.

- 3. Employer Contributions: Many employers contribute to their employees’ HSAs as part of their benefits package. According to the 2022 Employee Benefit Research Institute (EBRI) report, about 30% of employers offered HSA contributions, with the average employer contribution being around $800 for family coverage.

HSA Utilization Trends

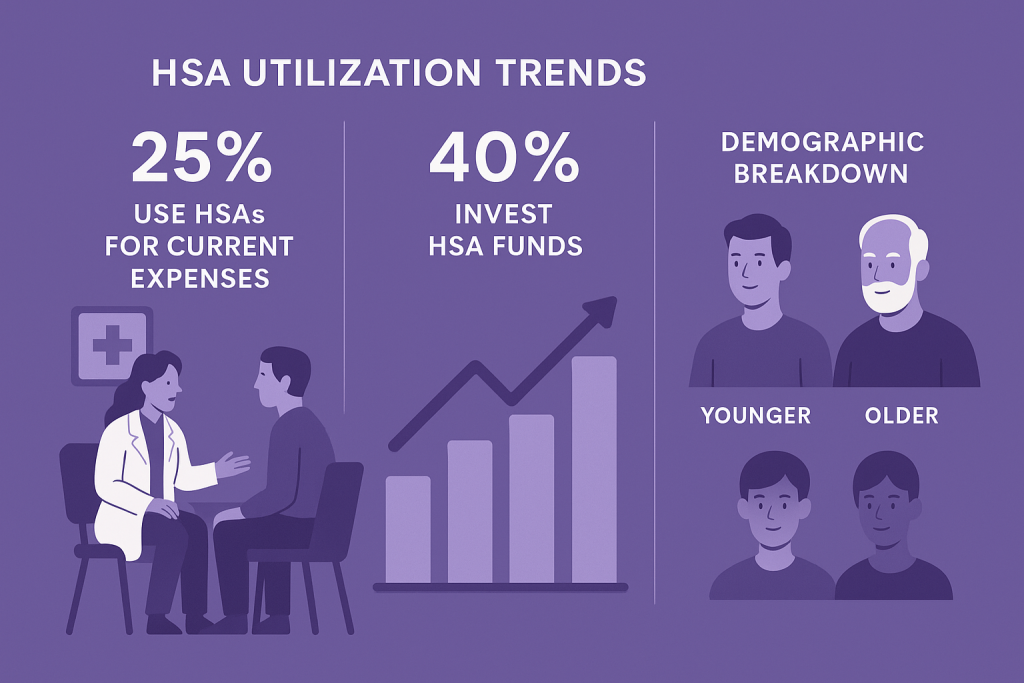

1. Utilization Rates: Despite the growth in accounts, utilization rates of HSAs remain varied. The EBRI reports that about 25% of individuals with HSAs use their accounts to pay for current medical expenses, while others may choose to save for future healthcare costs.

2. Investment of HSA Funds: A significant portion of HSA holders chooses to invest their funds for long-term growth. According to Devenir, nearly 40% of HSA account holders invest their HSA assets in mutual funds or other investment vehicles, highlighting a trend toward using HSAs as a retirement savings tool in addition to a healthcare expense account.

3. Demographics of HSA Users: Participation and utilization rates can vary significantly by demographic factors. Younger, healthier employees tend to participate in HSAs more than older workers, who may have higher medical expenses. A survey by the National Center for Health Statistics found that individuals aged 18-34 were more likely to have HSAs compared to those aged 45 and above.

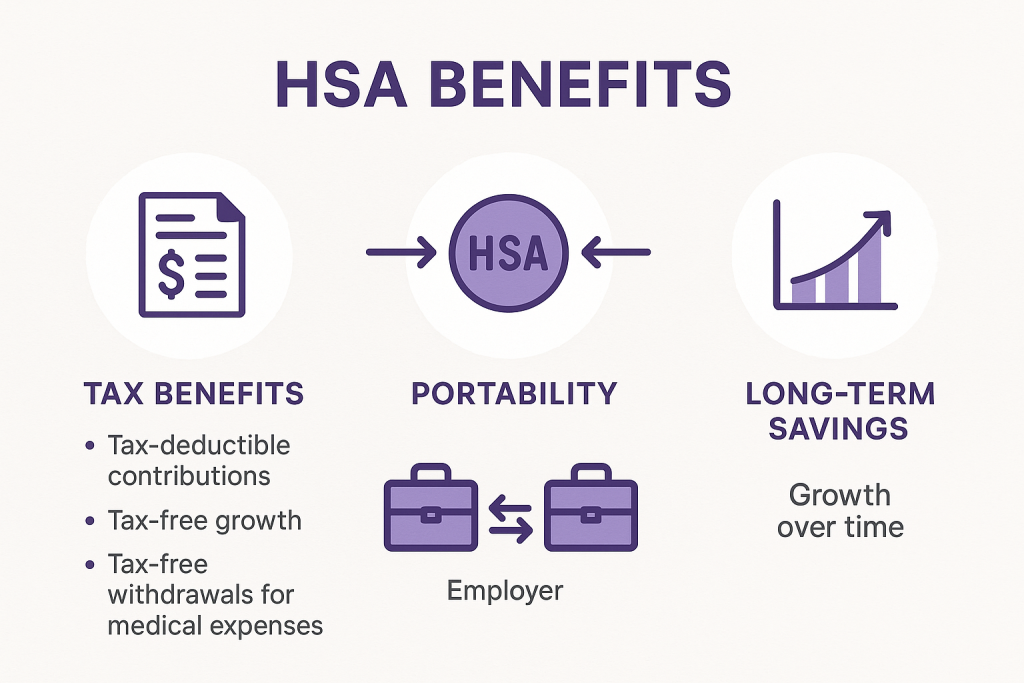

Advantages of HSAs

1. Tax Benefits: HSAs offer triple tax advantages: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. This makes HSAs one of the most tax-efficient ways to save for healthcare costs.

2. Portability: HSAs are owned by the individual, meaning they are not tied to a specific employer. Employees can take their HSA with them when they change jobs or retire, providing flexibility and continuity in healthcare savings.

3. Long-Term Savings Potential: HSAs can be used as a long-term savings vehicle, allowing individuals to save for healthcare expenses in retirement. Many financial advisors recommend using HSA funds for qualified expenses only after retirement, allowing the account to grow tax-free.

Challenges and Barriers

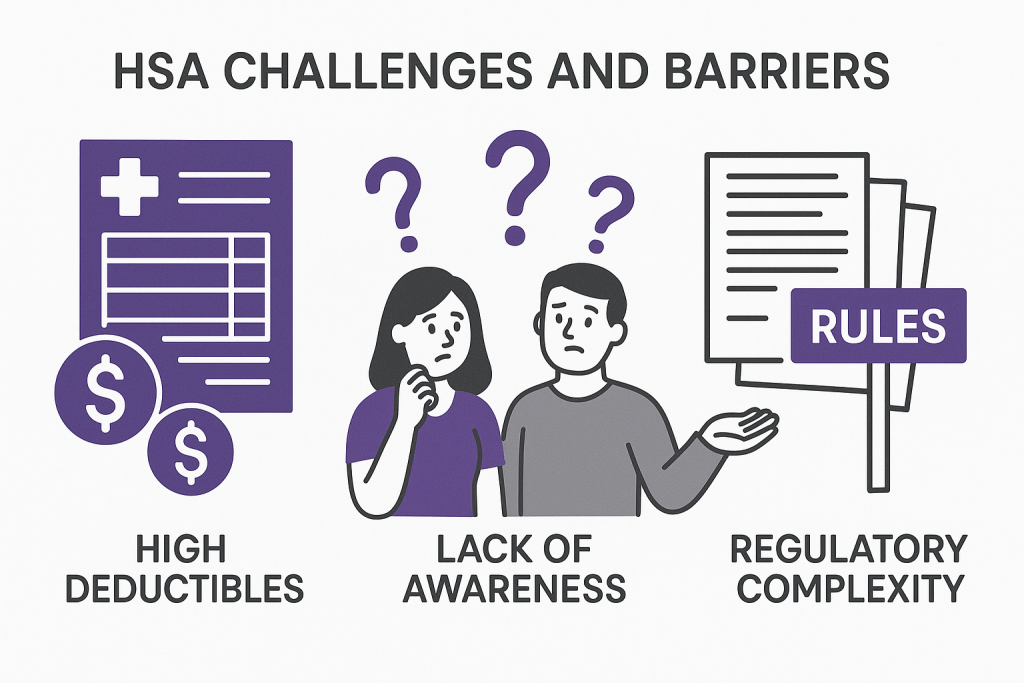

Despite their advantages, several challenges hinder the widespread adoption and utilization of HSAs:

- 1. High Deductibles: The requirement to pair HSAs with high-deductible health plans can deter some employees from enrolling, particularly those who may not have the financial means to cover high out-of-pocket costs.

- 2. Lack of Awareness: Many employees remain unaware of the benefits of HSAs or how to effectively use them. Education and communication from employers can play a critical role in increasing participation.

- 3. Complexity of Regulations: The rules governing HSAs can be complex, leading to confusion among employees regarding contribution limits and qualified expenses.

Ready to Offer Better Healthcare Solutions?

At Hooray Health, we help employers provide comprehensive healthcare benefits that work for every type of employee – from hourly workers to full-time staff. Our plans complement HSA strategies while offering immediate, affordable care options.

$25 Per Visit

At in-network facilities

$0 Telemedicine

24/7 consultations

4,700+ Locations

Nationwide network

Conclusion

Health Savings Accounts represent a growing opportunity for U.S. employees to manage healthcare costs effectively. With increasing participation and utilization, HSAs are becoming an integral part of the employee benefits landscape. However, addressing barriers such as high deductibles and lack of awareness will be crucial to maximizing the potential of HSAs as a tool for financial health.

References

Devenir. (2022). 2022 Year-End HSA Market Statistics. Retrieved from Devenir Website- Employee Benefit Research Institute (EBRI). (2022). Health Savings Accounts: Trends and Statistics. Retrieved from EBRI Website

- National Center for Health Statistics. (2022). Health Insurance Coverage in the United States: 2021. Retrieved from NCHS Website